Can You Get a Mortgage for a Modular Home in Europe in 2026?

Let’s be realistic, for a lot of people looking at modular homes, the big question is – can you actually get a mortgage for modular home, and if so, how does it all work? You probably love the idea of faster build times, knowing exactly how much you’ll be spending, and a brand new, modern-looking house – but the one thing that’s always on your mind is, can you get a mortgage for a modular home just like a regular old house?

The good news is that, generally speaking, you should be able to get a mortgage for a modular home in Europe. But the details really depend on where you live, who you’re getting the mortgage from, and how your local council sees it. Now, some lenders seem to have an easier time assessing a modular home that has been installed and is ready to go, and meets all the local building regulations with no issues at all.

Before we go any further, though, just to be clear, this article is a general guide, not a substitute for proper financial or legal advice. The thing is, mortgage requirements can vary so wildly across Europe that you really need to get some solid advice from a qualified financial pro or the bank in your area before you make any decisions about getting a mortgage for modular home.

Understanding Modular Home Financing in Europe

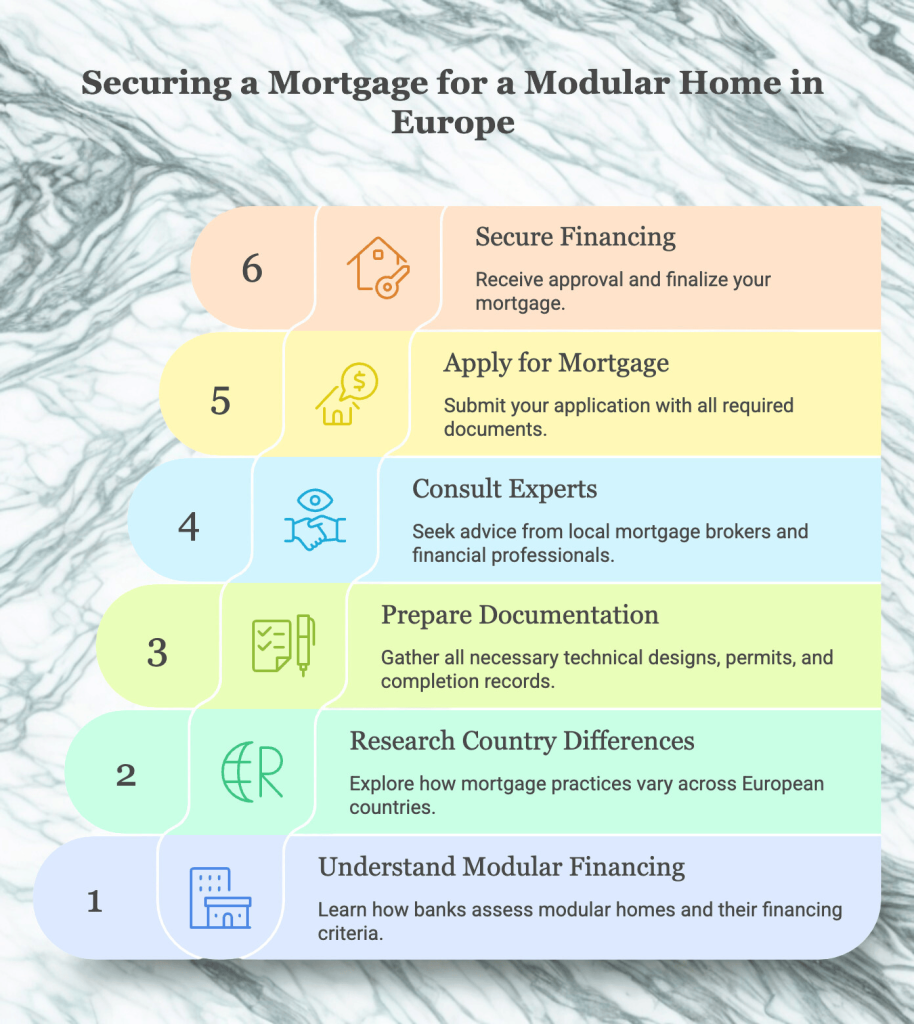

When banks assess a modular home, they are usually less concerned with the fact that it was built off-site and more focused on how the home functions as a property. One of the first questions lenders consider is whether the home is permanently installed or considered a movable structure. A modular home that is fixed to a certified foundation and intended for long-term residential use is far more likely to be treated similarly to a site-built house.

Foundation type also plays an important role. A permanent foundation signals durability and long-term value, which are key concerns for lenders. In addition, the way modular or prefabricated homes are classified under local law can affect how they are financed. Some countries distinguish clearly between residential buildings and temporary or transportable units, and this distinction matters when applying for a mortgage for modular home.

Turn-key modular homes are often viewed more favorably because they arrive fully finished. From a lender’s perspective, a completed home with installed systems, finished interiors, and clear documentation is easier to value and less risky than a partially finished project.

General Mortgage Basics in Europe

Although mortgage systems differ from country to country, many European lenders follow similar principles. Mortgages are usually based on the value of the property, the borrower’s income and credit profile, and the overall risk assessment of the loan. Loan terms, interest rates, and down payment requirements vary depending on national regulations and individual banks.

For readers interested in broader market insights rather than lender-specific rules, the European Mortgage Federation (EMF) publishes housing finance reports that outline mortgage trends across Europe. These reports, along with data from the European Central Bank (ECB), offer a useful high-level view of how housing credit works in the European context.

Country Differences: How Lenders View Modular Homes

Across Western Europe, including countries such as Germany, France, and the Netherlands, modular homes are increasingly recognized as standard residential properties when they are permanently installed and comply with local regulations. In these markets, lenders often rely heavily on professional appraisals and technical documentation to determine value. When the paperwork is clear and the home meets residential standards, modular construction itself is rarely a barrier.

In Nordic countries like Sweden and Denmark, prefabricated and modular housing has a long history. As a result, lenders in these regions are often more familiar with modular construction methods, particularly timber-based homes. This familiarity can make financing discussions more straightforward, provided that the home meets energy efficiency and zoning requirements.

This long-standing acceptance of prefabricated housing in the region is also closely linked to changing lifestyle needs, including the rise of multi-generational living across Nordic and Baltic countries. We explore this shift in more detail in our article on multi-generational modular living from Sweden to Estonia.

In Southern and Central Europe, mortgage practices can be more conservative and vary significantly by country. In some cases, lenders may require additional documentation or apply stricter valuation criteria, especially if modular housing is less common locally. This makes it especially important to consult local lenders or mortgage brokers who understand both national regulations and the modular housing market.

What Lenders Typically Look to Check Out

One of the biggest things lenders care about is whether the house sits on a solid foundation and has the proper building permits to go along with it. That lets them know the house is up to code, safe to live in, and intended to be someone’s home for a long time. Without all that in place, getting a loan can start to get really complicated.

Appraising the value of a house is a big part of the process, too. When a modular home is finally fixed in place, it gets treated pretty much like a regular house when it comes time to figure out how much it’s worth. An appraiser will usually look at comparable houses in the area, how well the house was built, how energy efficient it is, and where it’s located. Over in Europe, they’ve got their own rules of the road for this kind of thing, laid out by organizations like TEGoVA – they help make sure everyone’s on the same page.

Assessing the borrower’s financial situation is pretty much the same as it is for any mortgage. Income stability, existing debts, and credit history are all on the table, although the specifics can vary depending on the local banking rules and what the lender’s policy is.

How Turn-Key Modular Homes Can Help

Turn-key modular homes offer a clear advantage when it comes to financing because they reduce uncertainty. A fully completed home with finished interiors, installed electrical and plumbing systems, and documented specifications is easier for lenders to evaluate. From a risk perspective, a completed property is simpler to insure, appraise, and resell if necessary.

Clear documentation further supports the process. Technical design packages, approved permits, foundation plans, and completion records all help lenders understand exactly what they are financing. When these documents are readily available, it can make discussions with banks smoother and more transparent.

Other Financing Options to Explore

In some situations, buyers explore alternative or supplementary financing options alongside traditional mortgages. These can include construction loans or personal financing, depending on local regulations and lender offerings. Because these options vary widely across Europe, they should always be discussed with licensed professionals.

At a broader level, the European Commission provides general information about housing and consumer finance frameworks across EU member states. This information is readily available and can help readers understand the wider policy environment without focusing on individual financial products.

In addition, some countries offer green financing options or incentives for energy-efficient homes. While eligibility depends on national programs, energy performance is becoming an increasingly important factor in housing finance discussions across Europe.

Common Misconceptions About Modular Home Mortgages

A common misconception is that modular homes cannot be mortgaged at all. In reality, many modular homes qualify for financing when they are legally classified as permanent residential buildings. The construction method alone is rarely the deciding factor.

Another widespread belief is that modular homes are always more expensive to finance. In practice, modular home financing costs depend on the lender, market conditions, and documentation quality rather than whether a home is modular or traditionally built.

How to Prepare Before You Apply

Some buyers choose to explore mortgage pre-approval to better understand general eligibility and budget expectations. While pre-approval does not guarantee modular home financing, it can provide useful context early in the planning process.

Preparing documentation in advance is also helpful. This typically includes technical design packages, permit records, foundation and site plans, and model specifications. Having a clear overview of potential additional expenses can also improve financial planning. If you’re interested in this topic, you may find our recent article helpful: Modular Homes in Europe: The Hidden Costs of Waiting to Build.

Because mortgage practices vary widely, speaking with local mortgage experts who understand both national regulations and modular housing is one of the most effective ways to navigate the process.

Conclusion: Is It Possible to Get a Mortgage for Modular Home?

In most cases, the answer is yes. Modular home financing in Europe is generally possible, especially when the home is turn-key, permanently installed, and supported by clear documentation. However, outcomes depend heavily on the country, the lender, and local regulatory frameworks.

Since every situation is different, buyers should always seek guidance from licensed financial professionals and local lenders. With proper preparation and realistic expectations, modular homes can fit comfortably within standard European mortgage systems.